Contractor insurance is not just a document request. It is a control point before outside work, access, and payment begin.

Independent contractor insurance requirements depend on the work, contract, location, and risk the business is accepting. A remote designer does not create the same exposure as a field technician, a consultant handling sensitive data, or a subcontractor entering a warehouse.

This article is not legal or insurance advice. It is an operating guide for deciding what proof to request, who should approve it, and how to prevent expired insurance records from becoming a project, payment, or compliance problem.

What’s in this article?

- The insurance records businesses commonly request from independent contractors

- A practical review workflow before work starts

- A simple table for matching coverage checks to contractor risk

- Common mistakes that create avoidable exposure

- Where Workhint fits when insurance tracking needs to become a live workflow

Why contractor insurance requirements matter

Contractor insurance requirements matter because an independent contractor is usually operating as a separate business. If the work creates injury, property damage, professional error, data loss, vehicle risk, or a dispute, the hiring company needs to know whether responsibility, coverage, and documentation were addressed before work began.

Insurance also does not solve worker classification. The IRS explains that businesses must determine whether a worker is an employee or independent contractor based on the business relationship. The U.S. Department of Labor similarly focuses on the economic reality of the relationship under the FLSA.

The practical rule: review classification, scope, contract terms, and insurance together. Treat insurance as one gate in the contractor approval process, not as a substitute for legal, HR, finance, or risk review.

Independent contractor insurance requirements to check

There is no universal insurance package for every independent contractor. The right checklist should follow the risk of the work. A business may request one or more of the following:

| Coverage or record | When it matters | What to review |

|---|---|---|

| General liability | Work may cause bodily injury, property damage, or third-party claims | Policyholder name, effective dates, limits, exclusions, and certificate of insurance |

| Professional liability | Contractor gives advice, designs systems, handles financial work, or delivers expert services | Covered services, claim limits, retroactive dates, and contract alignment |

| Commercial auto | Contractor drives for the work or visits customer, field, or delivery locations | Vehicle use, policy dates, limits, and whether personal auto coverage is insufficient |

| Workers compensation or exemption | Contractor has employees, subcontractors, field crews, or state-specific coverage obligations | State rules, proof of coverage, exemption forms, and contract requirements |

| Cyber or data coverage | Contractor accesses customer data, systems, credentials, or sensitive records | Covered incidents, limits, exclusions, and security obligations |

Consumer-facing sources often tell contractors they may need general liability or professional liability insurance. For example, NerdWallet notes that many 1099 contractors need general liability, professional liability, or both, and that hiring companies may ask to see a certificate of insurance. From the business side, the point is to define coverage expectations based on the work being approved.

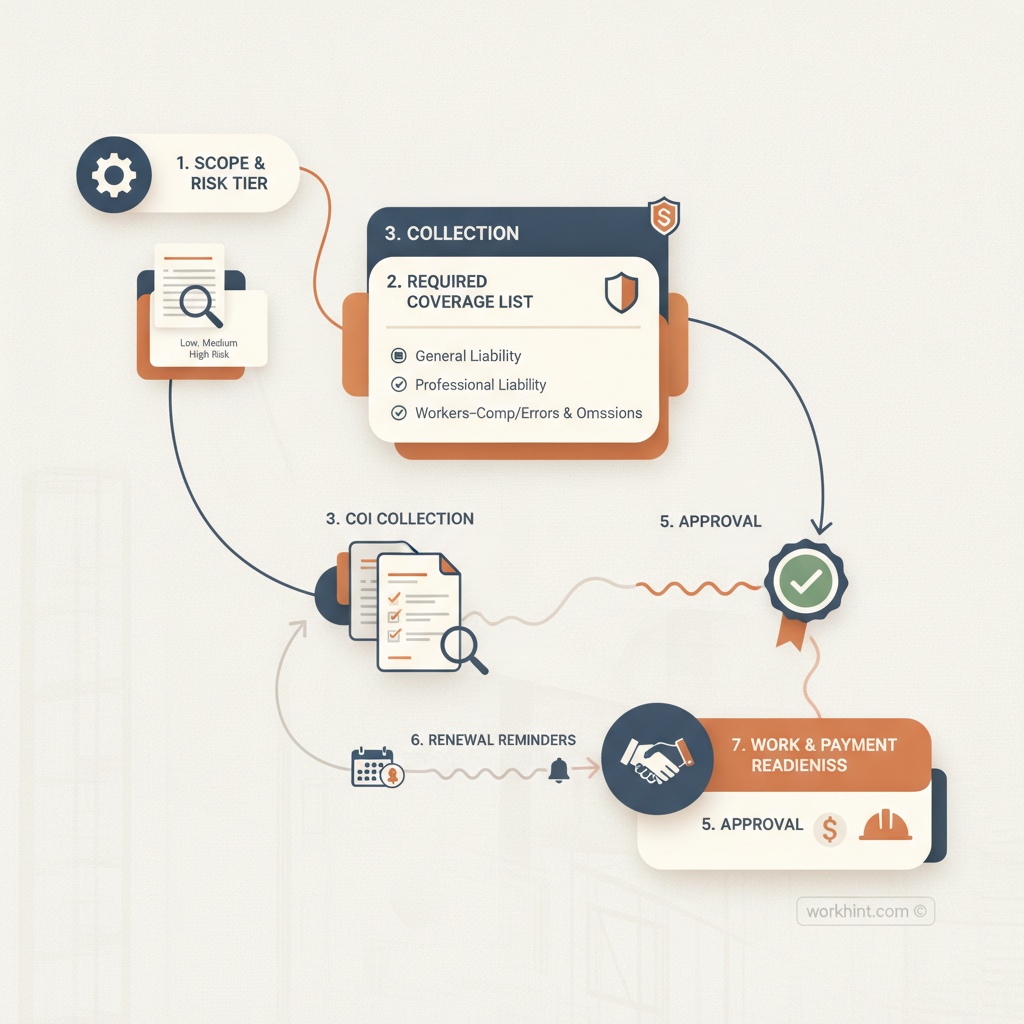

Contractor insurance workflow

A useful workflow prevents two failures: asking every contractor for unnecessary paperwork, and letting high-risk work begin with missing or expired coverage. Use this sequence before activating a contractor.

- Define the work and risk tier. Document what the contractor will do, where they will do it, what systems they will access, and whether they will interact with customers, equipment, property, vehicles, or regulated data.

- Set insurance requirements before contracting. Put required coverage, limits, additional insured language, waiver requirements, or exemption documentation in the agreement or statement of work where appropriate.

- Collect the certificate of insurance. Travelers advises asking for a certificate of insurance and checking the insurance company, policy number, and limits. For material risk, verify coverage with the insurer or broker instead of relying only on an emailed PDF.

- Assign the review owner. Operations may own completeness, legal may own contract terms, finance may own payment risk, and risk or insurance may own coverage adequacy.

- Block activation until approval is complete. Do not provision systems, assign field work, schedule customer visits, or release purchase orders until required records are approved.

- Track expiration dates. Insurance records should have renewal reminders. If a certificate expires mid-engagement, the workflow should flag the contractor before more work is assigned.

- Tie status to payment and renewal. Missing coverage should not become a surprise during invoice review. Keep status visible alongside scope, milestones, approvals, and payment readiness.

Practical ownership model

The easiest way to make contractor insurance reliable is to assign ownership by decision type.

| Owner | Decision | Output |

|---|---|---|

| Business owner | What work is being requested and why | Scope, location, deliverables, and risk context |

| Legal or procurement | What contract terms and insurance clauses apply | Agreement, SOW, required limits, and vendor obligations |

| Risk, finance, or operations | Whether proof is complete and current | Approved COI, exemption record, renewal date, and exceptions |

| IT or systems owner | Whether access can be provisioned | Role-based access only after approval |

| Finance | Whether work and invoices are payment-ready | Payment status connected to approved work and current records |

Common mistakes to avoid

- Using insurance as a classification shortcut. Insurance is relevant, but it does not decide whether someone is properly treated as an independent contractor.

- Requesting the same coverage from everyone. A low-risk remote specialist may not need the same records as a field service subcontractor.

- Collecting COIs without reading them. Check names, dates, limits, policy types, and whether the certificate matches the contracting entity.

- Forgetting state-specific rules. Workers compensation and contractor coverage rules vary. For example, the Colorado Department of Labor explains contractor coverage and rejection-of-coverage concepts for that state. Other states may differ.

- Letting expired records sit unnoticed. A certificate collected once is not enough for long-running engagements.

Where Workhint fits

Workhint fits when contractor insurance needs to become part of the external workforce operating system, not a spreadsheet tab or inbox search. A business can use Workhint to create contractor intake forms, assign risk tiers, collect insurance documents, route reviews to legal, finance, operations, or risk owners, block activation until approvals are complete, track expiration dates, and keep status visible alongside scope, assignments, access, milestones, invoices, and payment readiness.

The value is not that every contractor needs a heavy process. The value is that the process can adjust to the contractor type. Low-risk remote work can move quickly. Higher-risk field, customer-facing, vehicle, data, or regulated work can require deeper review before the contractor starts.

FAQ

What insurance should an independent contractor have?

It depends on the work. Common coverage types include general liability, professional liability, commercial auto, workers compensation or exemption documentation, and cyber or data coverage. The business should set requirements based on scope, location, customer exposure, data access, and contract risk.

Should a business ask for a certificate of insurance?

Yes, when insurance is relevant to the work. A certificate of insurance helps confirm the carrier, policy type, limits, named insured, and effective dates. For material risk, the business should verify details rather than simply storing the certificate.

Does insurance prove someone is an independent contractor?

No. Insurance may support the idea that the contractor operates as a separate business, but classification depends on the actual relationship. Review control, independence, payment terms, tools, scope, and applicable law.

Who should approve contractor insurance?

Ownership usually depends on the company. Operations can check completeness, legal can review contract terms, risk or finance can review coverage adequacy, and the business owner can confirm the work should proceed.

Conclusion

Independent contractor insurance requirements work best when they are tied to the real risk of the work. Define the scope, decide what coverage matters, collect and verify proof, assign reviewers, block work until approval is complete, and track renewal dates. When insurance status is connected to onboarding, access, assignments, and payment, the business can move faster without losing control of avoidable risk.

Leave a Reply