The difference is not just worker type. It is who owns contract, scope, payment, and operational risk.

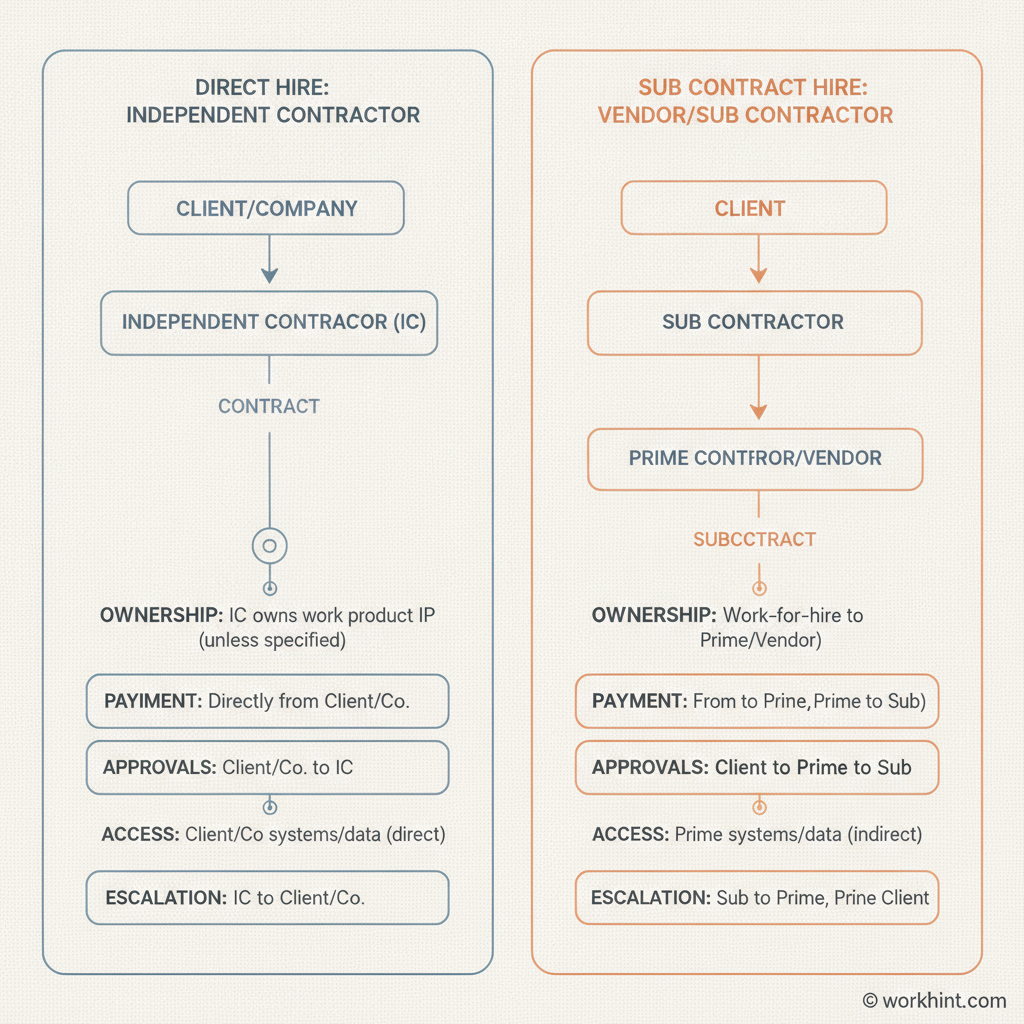

Independent contractor vs subcontractor is a common question because both can describe non-employee work. The practical difference is the contract chain. An independent contractor usually contracts directly with the business that needs the work. A subcontractor is hired by another contractor, agency, vendor, or prime provider to complete part of that larger obligation.

That distinction matters when work spans clients, vendors, project owners, and external specialists. Treat every outside worker the same and the business can lose track of approval, quality, payment, compliance records, and delivery accountability.

What’s in this article?

- The difference between independent contractors and subcontractors.

- How contract ownership, payment, supervision, and risk differ.

- A decision table for choosing the right operating model.

- A setup workflow for managing both.

- Common mistakes that create compliance, payment, or delivery problems.

Independent Contractor vs Subcontractor: The Core Difference

An independent contractor is an outside person or business hired to produce a result under a contract. The IRS explains that independent contractor status depends heavily on whether the payer controls only the result of the work, rather than controlling how the work is performed. Businesses should review the actual relationship, not just the label in the agreement, using official guidance such as the IRS page on independent contractor status.

A subcontractor is also outside the client company’s employee structure, but the relationship is one step removed. Cornell Law’s Wex definition describes a subcontractor as an outside company or individual hired by a general contractor to perform part of work under an existing client contract.

In plain terms: if your company hires a freelance designer directly, that person is an independent contractor. If your company hires a marketing agency and that agency hires the designer for part of the campaign, the designer is a subcontractor to the agency.

Comparison Table for Business Teams

| Question | Independent Contractor | Subcontractor |

|---|---|---|

| Who hires them? | Your company hires them directly. | A contractor, agency, vendor, or prime provider hires them. |

| Who owns the primary relationship? | Your company manages the relationship and contract. | The prime contractor or vendor usually manages the subcontractor relationship. |

| Who defines scope? | Your company and the contractor agree on scope. | The subcontractor’s scope should map to part of the prime contract or statement of work. |

| Who pays them? | Your company pays the contractor according to the contract. | The prime contractor or vendor usually pays the subcontractor. |

| Who handles performance issues? | Your company addresses issues directly with the contractor. | Your company usually escalates through the prime contractor unless the contract says otherwise. |

| Main operational risk | Misclassification, unclear deliverables, missing tax records, access sprawl. | Hidden work, unclear accountability, unmanaged access, weak flow-down requirements. |

How to Decide Which Model Fits the Work

Use a direct independent contractor relationship when the business wants a named specialist, direct scope control, direct communication, and a clear payment relationship. This is common for consultants, creative freelancers, fractional operators, technical specialists, and project-based professionals.

Use a subcontractor model when the business buys an outcome from a prime vendor, agency, staffing partner, or general contractor, and that provider needs other specialists to deliver. The client should focus less on daily task control and more on vendor accountability, reporting, approval rights, security rules, and quality thresholds.

The U.S. Department of Labor’s FLSA employment relationship guidance is a useful reminder that worker classification depends on the economic reality of the relationship. This article is operational guidance, not legal advice. For classification, tax, employment, licensing, or cross-border questions, review the facts with counsel or a tax advisor.

A Workflow for Setting Up Either Relationship

- Define the business outcome. Write the result, acceptance criteria, deadline, budget, and evidence required to prove completion.

- Identify the contract chain. Confirm whether your company is contracting directly with the worker or through a prime contractor, agency, or vendor.

- Assign ownership. Name the business owner, approver, finance owner, security owner, and escalation contact.

- Collect the right documents. For direct contractors, this may include agreement, tax form, payment details, insurance, credentials, and confidentiality terms. For subcontractors, make sure the prime agreement covers subcontracting rights, approval rules, data access, and flow-down obligations.

- Set access boundaries. Give external workers only the systems, locations, files, and channels needed for the approved scope.

- Track deliverables, not employee-style activity. Use milestones, outputs, quality checks, approvals, and issue logs instead of managing the worker like an employee.

- Connect payment to approval. Do not release payment simply because time passed. Tie invoices to accepted work, milestone evidence, or approved service records.

- Close the loop. At the end, remove access, collect files, resolve invoices, and store the relationship history.

Common Mistakes to Avoid

The first mistake is assuming a subcontractor is invisible to the client business. Even when the prime contractor owns the relationship, your company may still care about access, confidentiality, insurance, safety, data handling, customer communication, and brand standards.

The second mistake is directing subcontractors as if they are your own staff while the prime contractor remains responsible on paper. If you need direct control, direct approvals, or direct assignment, the agreement should reflect that reality.

The third mistake is treating a direct contractor like an employee. The IRS notes that businesses should consider behavioral control, financial control, and the relationship of the parties when evaluating worker status. See the IRS guidance on independent contractor or employee classification before building a process that looks like employment in practice.

Where Workhint Fits

Workhint fits when a company needs an operating layer for external work. For direct contractors, Workhint can structure intake, onboarding, documents, permissions, assignments, approvals, payment status, reminders, and reporting around each engagement. For subcontracted work, Workhint can help map the prime vendor relationship, approved subcontractor roles, access rules, deliverable checkpoints, escalation paths, and payment approval evidence.

The value is not replacing legal review or vendor agreements. It is turning the chosen model into a repeatable workflow so operations, finance, security, and business owners can see who is approved, what they can access, what they owe, and what has been accepted.

FAQ

Is a subcontractor the same as an independent contractor?

Not exactly. A subcontractor can be an independent business or self-employed worker, but the operational distinction is that they are hired by another contractor or vendor to perform part of a larger contract.

Can a company pay a subcontractor directly?

Sometimes, but it depends on the contract structure. Direct payment can change accountability, tax reporting, insurance requirements, and approval rights. Finance and legal teams should review the arrangement before changing the payment path.

Who is responsible for subcontractor quality?

The prime contractor or vendor is usually responsible to the client for the subcontracted work. The client should still define quality standards, approval gates, reporting requirements, and escalation rules in the prime agreement.

Do independent contractors and subcontractors receive Form 1099-NEC?

U.S. reporting depends on who pays whom, payment amount, entity type, and other tax rules. The IRS provides guidance on reporting payments to independent contractors, but businesses should confirm details with a tax advisor.

Which model is better for scaling external work?

Direct contractors give more visibility and control. Subcontractor models can scale delivery through vendors or agencies, but they require stronger contract-chain governance. The better model depends on whether the business needs direct specialist control or outsourced delivery accountability.

Conclusion

The difference between an independent contractor and a subcontractor is not just a label. It changes who owns the relationship, defines the work, pays, approves, and manages risk. Map the contract chain first, then build the workflow around ownership, scope, documents, access, approvals, and payment.

When that structure is clear, external work becomes easier to coordinate. Contractors know what result they owe, vendors know what they own, and internal teams know who can approve work, release payment, and close the engagement.

Leave a Reply