Contractor payments work when terms, approvals, tax records, and payment status live in one repeatable process.

How to pay independent contractors is not just a finance question. A company has to confirm the worker is being treated correctly, collect tax information, define terms, approve work, release payment, answer questions, and keep records for year-end reporting.

The exact rules depend on the country, worker, contract, payment method, and business model. This article focuses on the practical workflow a U.S. business can use when paying domestic independent contractors. It is not legal or tax advice.

What’s in this article?

- The documents to collect before payment

- How to set clear payment terms

- A step-by-step contractor payment workflow

- A comparison of common payment methods

- Common mistakes that create payment delays or compliance risk

- Where Workhint fits when contractor payments become operationally complex

Why contractor payments need a workflow

Contractors are not paid like employees. Employee payroll usually runs on a fixed cycle with withholding, benefits, and payroll records already connected. Contractor payments often depend on invoices, milestones, completed jobs, approved hours, service reports, project deliverables, or customer acceptance.

That means payment accuracy depends on several people doing their part. The contractor needs clear terms. The manager confirms work. Finance needs the tax form, approval, payment method, vendor record, and payment date. Operations needs visibility when payments are blocked or disputed.

Before any payment process starts, confirm the worker relationship. The IRS says worker classification depends on control and independence, and the Department of Labor’s FLSA employment relationship guidance describes an economic reality test for worker status.

What to collect before work starts

Do not wait until the first invoice arrives to collect payment information. Make contractor setup part of onboarding.

For U.S. contractors, the IRS explains that Form W-9 is used to provide a correct taxpayer identification number for information returns. The IRS page on forms and associated taxes for independent contractors also explains that Form 1099-NEC is used for reportable nonemployee compensation, with some withholding situations possible.

A practical setup should include the signed agreement or statement of work, tax documentation, legal name, business name if applicable, address, payment method, invoice requirements, payment timing, approval owner, dispute process, and any required insurance or compliance records.

Set contractor payment terms clearly

Payment terms should be written before work begins. Vague terms like “paid after completion” create confusion when work has multiple deliverables, revisions, or sign-offs.

Typical contractor payment terms often use Net 10, Net 15, Net 30, or Net 60 after invoice receipt or approval. OnPay’s overview of typical payment terms for contractors notes that terms vary by contract. The operational point is to define the trigger: invoice date, invoice receipt, deliverable acceptance, manager approval, or the next payment run.

| Term | Best use | Operational risk |

|---|---|---|

| Due on receipt | Small one-time work, urgent jobs, trusted specialists | Finance may not have enough review time if approvals are manual |

| Net 10 or Net 15 | Fast-cycle contractors, creative work, field services, recurring contributors | Delays happen quickly if invoice rules are unclear |

| Net 30 | Standard vendor-style payments and monthly invoice cycles | Contractors may deprioritize work if payment feels slow or opaque |

| Milestone-based | Projects with defined deliverables, phases, or acceptance criteria | Payment disputes increase if acceptance criteria are vague |

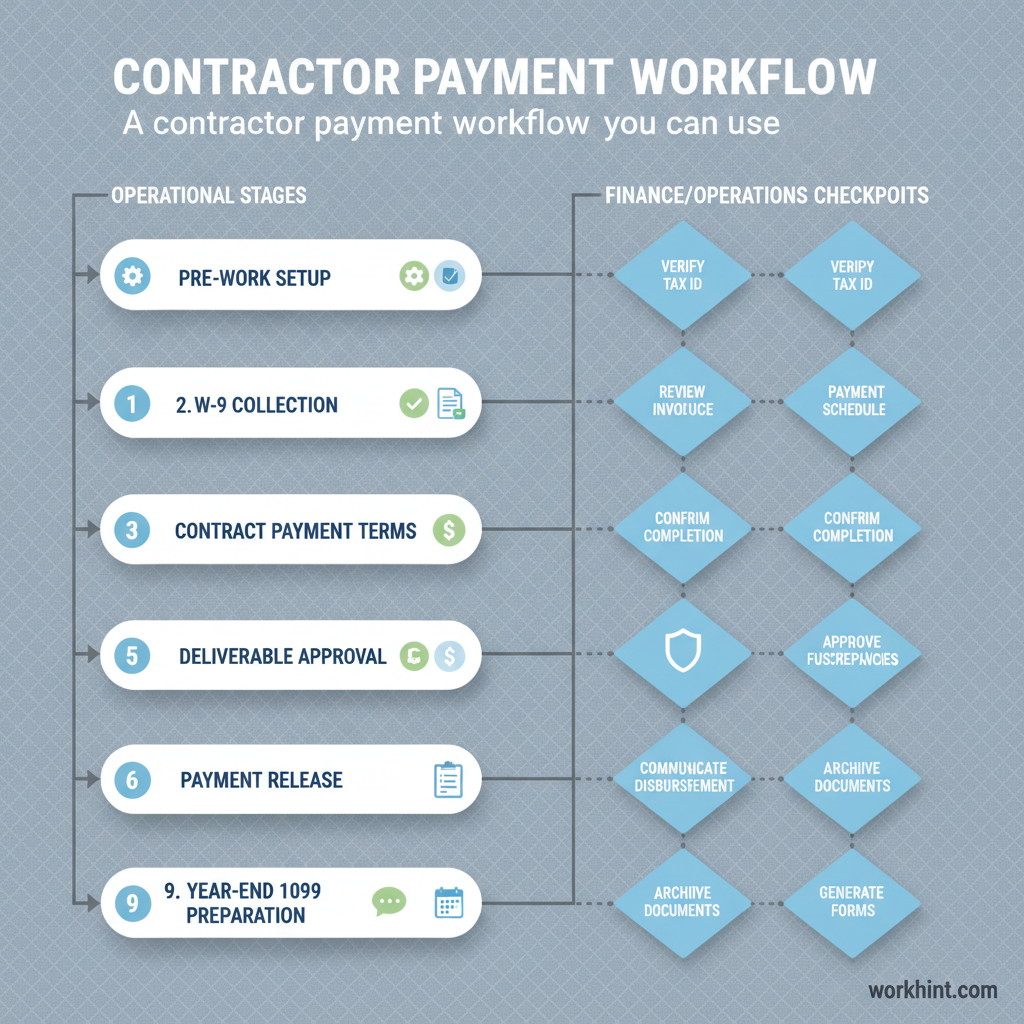

A contractor payment workflow you can use

- Confirm the engagement model. Decide whether the work should be handled by a contractor, vendor, agency, employee, or another arrangement. Route unclear cases to legal, HR, or finance.

- Create the contractor record. Collect the signed agreement, payment terms, tax form, payment method, contact details, and approval owner before work begins.

- Define what triggers payment. Tie payment to an invoice, milestone, completed job, approved timesheet, service report, accepted deliverable, or scheduled payment run.

- Receive the invoice or payment request. Require consistent invoice fields: contractor name, invoice number, dates, project or job reference, amount, payment method, and supporting detail.

- Verify the work. The manager or operations owner confirms the deliverable, hours, service visit, customer acceptance, or milestone completion.

- Review exceptions. Route missing tax forms, wrong rates, duplicate invoices, disputed work, chargebacks, advances, or deductions to the right owner before payment release.

- Approve and pay. Finance releases payment through the agreed method and records the payment date, amount, reference number, and status.

- Keep year-end records current. Track payments throughout the year so 1099-NEC preparation is not rebuilt from scattered spreadsheets.

Choose the right payment method

The best payment method depends on contractor preference, cost, geography, payment speed, record quality, and finance controls. For U.S. contractors, ACH and bank transfer are common for recurring payments. Checks still work but create mailing delays. Cards, PayPal, and payment apps can be useful but may create fees or weaker internal controls.

For international contractors, do not assume the domestic workflow is enough. Cross-border payments may involve local labor rules, tax forms, withholding, currency conversion, local banking rails, sanctions screening, and data handling requirements. The safest approach is to treat global contractor payments as a separate workflow with specialist review.

Common contractor payment mistakes

- Paying before setup is complete. Missing tax forms, agreements, and payment details create cleanup work later.

- Using unclear payment triggers. “After completion” is not specific enough when work has revisions, approvals, or partial delivery.

- Letting every manager invent their own process. Different invoice rules create inconsistent contractor experience and finance exceptions.

- Mixing contractor payments with employee payroll habits. Contractors need business payment records, not employee-style payroll assumptions.

- Waiting until January to organize 1099 records. The IRS page for Form 1099-NEC makes clear that nonemployee compensation has its own reporting form. Keep records clean during the year.

Where Workhint fits

Workhint fits when contractor payment is part of a larger external workforce workflow. A company can use Workhint to connect contractor intake, onboarding documents, role-based access, agreements, assignments, deliverable review, invoice approval, exception routing, payment status, compliance reminders, and reporting.

That matters when contractors are spread across departments, projects, field work, service delivery, marketplaces, agencies, or global teams. Instead of chasing approvals, the workflow can show which contractor is approved, what work is complete, what invoice is waiting, who needs to sign off, and which payments are ready.

FAQ

What is the best way to pay independent contractors?

The best method is usually the one that matches the contract, creates a clear payment record, works for the contractor, and fits finance controls. ACH or bank transfer is common for recurring U.S. contractors, while international payments may require a specialist payment workflow.

Do independent contractors need to submit a W-9?

U.S. businesses commonly request Form W-9 from U.S. contractors so they have taxpayer identification information for reporting. Confirm requirements with a tax professional when the contractor, entity type, or location is unclear.

When should a contractor be paid?

Contractors should be paid according to the written agreement. The key is to define whether the due date starts from invoice date, invoice receipt, deliverable acceptance, manager approval, or a scheduled payment run.

Can a business pay contractors through payroll?

Contractors are generally not handled like employees in payroll because they are not paid wages with the same withholding and benefits structure. Some payroll platforms support contractor payments, but the records, tax forms, and workflow are different.

What happens if contractor information is missing?

Do not improvise. Route the payment to an exception process, request the missing agreement, tax form, invoice details, or payment method, and document the resolution before releasing payment.

Conclusion

Paying independent contractors well is less about choosing one payment app and more about building a clear operating workflow. Start before work begins, collect the right records, define payment terms, connect invoices to approvals, resolve exceptions visibly, and keep payment data ready for reporting. Contractors get a better experience, managers know what they must approve, and finance avoids rebuilding the process at the end of every month.

Leave a Reply